Retirement . . . Ready or Not!

If you’re retired, or soon to be, you’re likely a Canadian baby-boomer. You are seeking more information about your retirement beyond merely finances, and advisors are uniquely positioned to provide you with additional retirement insight and planning.

Currently, Canadians aged 65 years old, can expect to live an additional 22 to 24 years, on average. Not only are people living longer, they are leading more active retirements. Achieving success in retirement no longer requires the bills to be paid, and to sit at home awaiting the arrival of the grim-reaper!

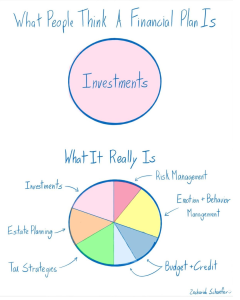

To gain access to the investable assets today, and manage them into retirement, advisors should examine their clients in a broader, more complete perspective.

What you need to know

| Retirement Element | Ready to Retire | Not Ready |

|---|---|---|

| Vision | *Unified view of retirement by both partners *Active/equal trade-offs *No Surprises *Guided decision-making for all Retirement Elements | *Costly and scattered decision-making for other elements (below) *Delayed decision-making for investments and accounts *Anxiety over end-of-work |

| Health | *Health considerations not informing Interests, Social or Lifestyle elements *Critical Illness, healthcare benefits and/or savings in-place | *Successful and active retirement unattainable if health matters are not addressed, fitness promoted *Unpredictable and high healthcare costs could financially cripple retirement |

| Interests and Social | *Activities and friends independent from work, or maintained by choice *Increasing curiosity for hobbies and relationships | *Little or no plans to fill approximately 2,000 hours per year previously spent at-work *Boredom leading to increased health risks |

| Lifestyle | *Activities of daily living planned for all life-stages *Living integrated with family and friends, along with mutual activities and family events | *Days passing from one to the next without purpose, interaction or accomplishment |

| Home | *Accommodation needs understood for various phases of retirement, mobility and wellness *Costs anticipated, free capital identified *Vacation home transfer planned, with life insurance if necessary | *Home does not match Interests, Social or Lifestyle needs *Costly modifications avoided that could improve quality of life *Inexpensive modifications not planned, destroying peace of mind and quality of life |

| Legacy | *Final wishes to be followed *Tax liability at time of transfer accounted for with insurance, for example, and/or planned *Wills, Powers of Attorney considered and constructed to fulfill final wishes precisely | *Unequal or missed distribution of assets and heirlooms *Tax surprises require disposition of assets (like family cottages) to pay terminal return *Tax bill nominally higher without planned giving while alive |

The Bottom Line

Without planning that includes more elements than just finances, retirement and the years leading up to it can be anxiety laden. The period that should be relatively carefree will be the opposite.

Financial planning is a critical element of all retirement plans, but an analysis that focuses solely on money will not prepare you for a successful retirement. Additional items like those mentioned above must also be addressed.