Is Your Financial Life Jacket Onboard?

“Is Your Financial Life Jacket Onboard?”

By: Rushit Goyani, RFRA

Storms don’t announce themselves. The same goes for financial disruption. So, when life gets choppy—are you wearing your financial life jacket, or are you just hoping to swim?

The market can be like the ocean—sometimes calm, sometimes wild, and sometimes, out of nowhere, a wave hits. And when that happens, you better have your life jacket on.

In the world of investing, your life jacket isn’t made of foam or nylon—it’s made of preparation. Two to three years’ worth of financial savings, kept aside for emergencies—medical, personal, or otherwise. It’s money that’s liquid and accessible, ideally in a conservative portfolio that doesn’t nosedive during a market dip but still grows more than inflation. That’s the peace of mind you need.

Last week, we saw the market fluctuate wildly—up 8–10% one day, down 6–7% another. By the end of it, we will back to square one. But for many investors, those swings triggered fear. Portfolios dropped, emotions ran high, and panic set in.

But not for everyone.

The investors who stayed calm? They were the ones with their life jackets on. They weren’t worried because they had their emergency funds in place. They knew that regardless of what happens in the market—or what headlines pop up—they’ll still eat good food, drive their nice cars, take vacations, and live their lives. Nothing fundamentally changes for them.

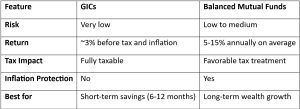

Now, let’s be clear: we’re not suggesting you pull everything and stash it in GICs. That doesn’t work either. GICs barely beat inflation, if at all. They might seem “safe,” but you’re losing money in the long term because your cash isn’t working for you. It’s just sitting there. Not ideal.

This is where a good financial planner enters the picture. At ECIVDA, we work with clients to design portfolios that reflect their risk tolerance and future needs. We call to check in, support you during turbulent times, and make sure your financial “life jacket” is always zipped up and ready.

Because when the market gets rough—and it will—those with a solid foundation don’t flinch. They float.

If you don’t have this kind of setup yet, don’t worry. We’re here to help.

Click HERE to book a meeting today!!